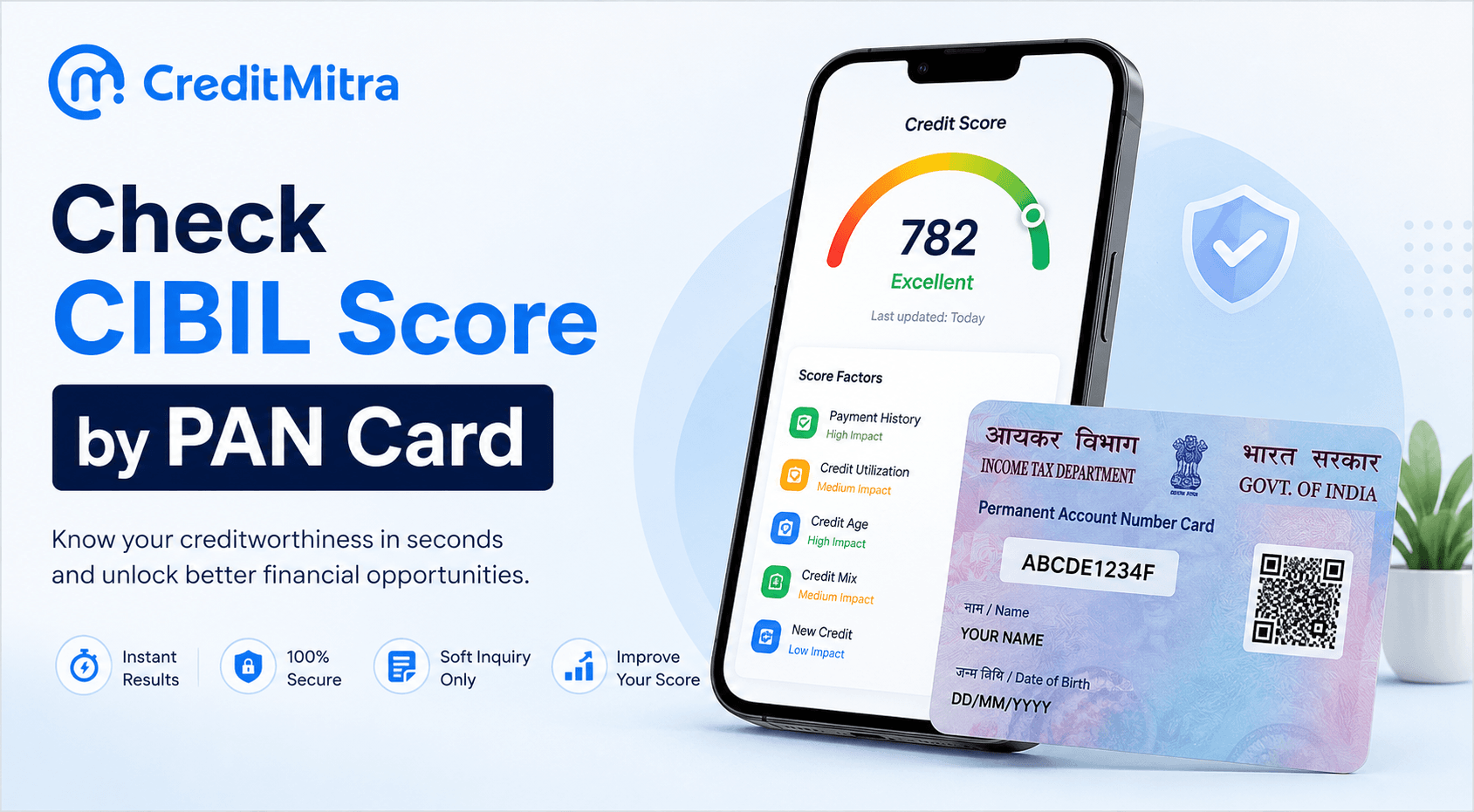

Check CIBIL Score by PAN Card: Complete Step-by-Step Guide 2026

Summarize with AI

You want to check your CIBIL score before applying for a personal loan.

And, You have your PAN card. You assume you can check instantly without anything else.

You’re surprised when the website asks for OTP verification.

“Why do I need OTP if I’m using my PAN card?” you think.

Here’s the complete guide to checking CIBIL score by PAN card, explaining why OTP is required, how to do it in 5 minutes, and how to use this information smartly.

Can You Check CIBIL Score by PAN Card Alone?

Short answer: No. Your PAN card is essential, but insufficient.

Why: While PAN uniquely identifies you, it’s not enough to prove you’re the actual account holder. Anyone with access to your PAN (visible on tax returns, salary slips, rent agreements) could potentially access your credit report.

Banks and CIBIL require OTP verification as a mandatory security step. This ensures only you access your sensitive financial data.

Reality check: If any website claims to let you check CIBIL score by PAN card without OTP, it’s either:

- Operating outside regulatory guidelines

- Using outdated information

- A potential scam

The RBI requires OTP verification for credit data access. No legitimate platform bypasses this.

Why OTP Is Mandatory (And Why It’s Good)

Think of it this way: Your PAN card is like your username. Your OTP is your password.

Just like you wouldn’t want anyone accessing your Gmail with just your email address, lenders don’t want anyone accessing your credit report with just your PAN.

OTP verification protects you from:

- Identity theft: Someone accessing your credit report fraudulently

- Unauthorized applications: Loan applications opened in your name

- Credit damage: Fake defaults reported to CIBIL in your name

The 10-minute OTP window ensures only you (with access to your registered phone) can view your data.

Read More: How to Read CIBIL Report

Step-by-Step: How to Check CIBIL Score by PAN Card (5 Minutes)

Method 1: Official CIBIL Website (Most Secure)

Step 1: Go to CIBIL Website

- Visit www.cibil.com

- Click “Get Your Free CIBIL Score”

Step 2: Create Account

- Enter email (this becomes your username)

- Create strong password

- Click “Register”

And, Step 3: Enter PAN Details

- Full name (as on PAN)

- Select “PAN Card” from ID Type dropdown

- Enter 10-digit PAN number

- Enter date of birth (must match PAN)

- Enter PIN code and state

- Enter registered mobile number

- Click “Accept and Continue”

Step 4: OTP Verification (Critical Step)

- CIBIL sends OTP to your registered mobile

- Enter OTP in the field

- OTP valid for 10 minutes

- Click “Continue”

And, Step 5: Optional Device Pairing

- CIBIL asks “Pair this device?”

- Choose “Yes” if personal device (laptop/phone)

- Choose “No” if public device (internet cafe/shared computer)

Step 6: View Your Score

- Screen shows “Successfully Enrolled!”

- Click “Go to Dashboard”

- Your CIBIL score displays (300-900 range)

- Full credit report also available

Time: 3-5 minutes total

Cost: FREE once per calendar year

Method 2: Via Bank’s Net Banking (Faster if You’re Already Logged In)

If you have account at HDFC/ICICI/SBI/AXIS:

- Log into your net banking account

- Look for “My CIBIL Score” or “Credit Score” section

- Click to view (no extra OTP needed, bank already verified you)

- Score displays instantly

Advantage: No extra OTP since bank already authenticated you

Disadvantage: Only works if you’re already logged in and have that account

Method 3: Third-Party Platforms (Paisabazaar, BankBazaar, etc.)

- Visit CreditMitra.in or similar platform

- Click “Check CIBIL Score”

- Enter PAN + basic details

- Receive OTP on mobile

- Enter OTP

- View score

Note: First time requires full details. Next time, just mobile + OTP.

What Information You Need to Check CIBIL Score by PAN

Mandatory:

- PAN card number (10 digits)

- Full name (exactly as on PAN)

- Date of birth (from PAN)

- Registered mobile number (linked to PAN)

- Email address

Optional:

- Address (PIN code, state)

- Employment details (may help if PAN has errors)

Having these ready before starting saves time.

What Your CIBIL Score Report Shows

When you check CIBIL score by PAN card, you get:

1. CIBIL Score (3-digit number: 300-900)

- 750+: Excellent (best loan rates)

- 700-749: Good (easy approvals)

- 650-699: Fair (possible rejections)

- Below 650: Poor (rejections likely)

2. Credit Report (CIR) with:

- Payment History: Your on-time/late payments for last 3 years

- Account Summary: All active loans, credit cards, amounts outstanding

- Personal Information: Name, PAN, addresses, employers

- Credit Inquiries: Hard inquiries from loan applications

- Credit Mix: Types of credit you use (loans, cards, etc.)

3. DPD (Days Past Due):

- Shows how many days late you were on payments

- 000 = on time, 030 = 30 days late, etc.

Read More: How to Check CIBIL Score in Minutes

Important: Checking Your Score Is a SOFT Inquiry

Myth: Checking your own CIBIL score damages it.

Truth: When you check your own score, it’s a soft inquiry and has zero impact on your CIBIL score.

Only hard inquiries (when lenders check during loan/credit card applications) temporarily lower your score by 5-10 points per inquiry.

You can check your CIBIL score unlimited times without any damage.

One Free Report Per Year (As Per RBI Rules)

Starting January 1, 2026, RBI allows:

- One detailed free CIBIL report per calendar year

- You can check anytime after that, but may need to pay (₹99-299 for detailed report)

- However, many platforms offer unlimited free checks anyway

Check once, review carefully for errors, then check again before major loan applications.

What If Your Registered Mobile Number Has Changed?

Problem: Mobile number on file doesn’t receive OTP

Solution:

- Visit CIBIL in person with original PAN + ID

- Update mobile number with CIBIL

- Or contact your bank to update it there (banks report to CIBIL)

- Takes 3-7 days for update to reflect

- Then retry CIBIL score check

Prevention: Keep your mobile number updated with your bank and PAN records.

Score Too Low? Next Steps (After Checking)

If your CIBIL score is below 700:

Don’t panic. But act immediately:

- Review your report for errors (wrong accounts, incorrect payment dates)

- Dispute errors with CIBIL (they investigate within 30 days)

- Improve your score: Pay all bills on time for 3-6 months

- Reduce credit card utilization to below 30%

- Wait 6-12 months for significant improvement

- Recheck your score before applying for loans

FAQ: CIBIL Score Check by PAN Card

Q: Can I check my spouse’s CIBIL score using his PAN card?

A: No. You cannot access anyone else’s credit report, even your spouse. Only that person can check their own score. This protects privacy.

Q: If I’m a student with no credit history, what will my score be?

A: No score appears. Lenders see “no data.” You don’t become reportable until you take your first loan/credit card. This is fine, not negative.

Q: How often should I check my CIBIL score?

A: Ideally once every 3-6 months to monitor for errors or fraud. At minimum, check 1 month before applying for major loans.

Q: Can I check CIBIL score using Aadhaar instead of PAN?

A: Yes, but you may get incomplete data. Most Indian lenders report using PAN, so Aadhaar-based checks might miss some accounts. PAN is more reliable.

Q: Does improving my CIBIL score take months or years?

A: Depends on damage level. Minor late payments: 6 months of on-time payments = 50+ point recovery. Major defaults: 18-24 months for full recovery.

Q: Should I improve CIBIL before applying for a personal loan?

A: If below 700, wait 3-6 months and improve. If 650+, apply to fintech lenders (easier approval). CreditMitra shows lenders accepting various CIBIL profiles without hard inquiry damage.

Using CIBIL Check for Smart Loan Applications

Once you know your CIBIL score:

If 750+:

- Apply directly to banks (you’ll get best rates)

- Use CreditMitra to compare rates with 30+ lenders

- Negotiate for lower interest based on excellent score

If 700-749:

- Compare fintech + NBFC options via CreditMitra

- Avoid multiple direct applications (each hard inquiry -5 points)

- One soft inquiry via CreditMitra = zero CIBIL damage

and, If 650-699:

- Fintech lenders your best option

- Expect rates 2-3% higher

- Use CreditMitra’s soft inquiry to find accepting lenders

- Avoid traditional banks for now

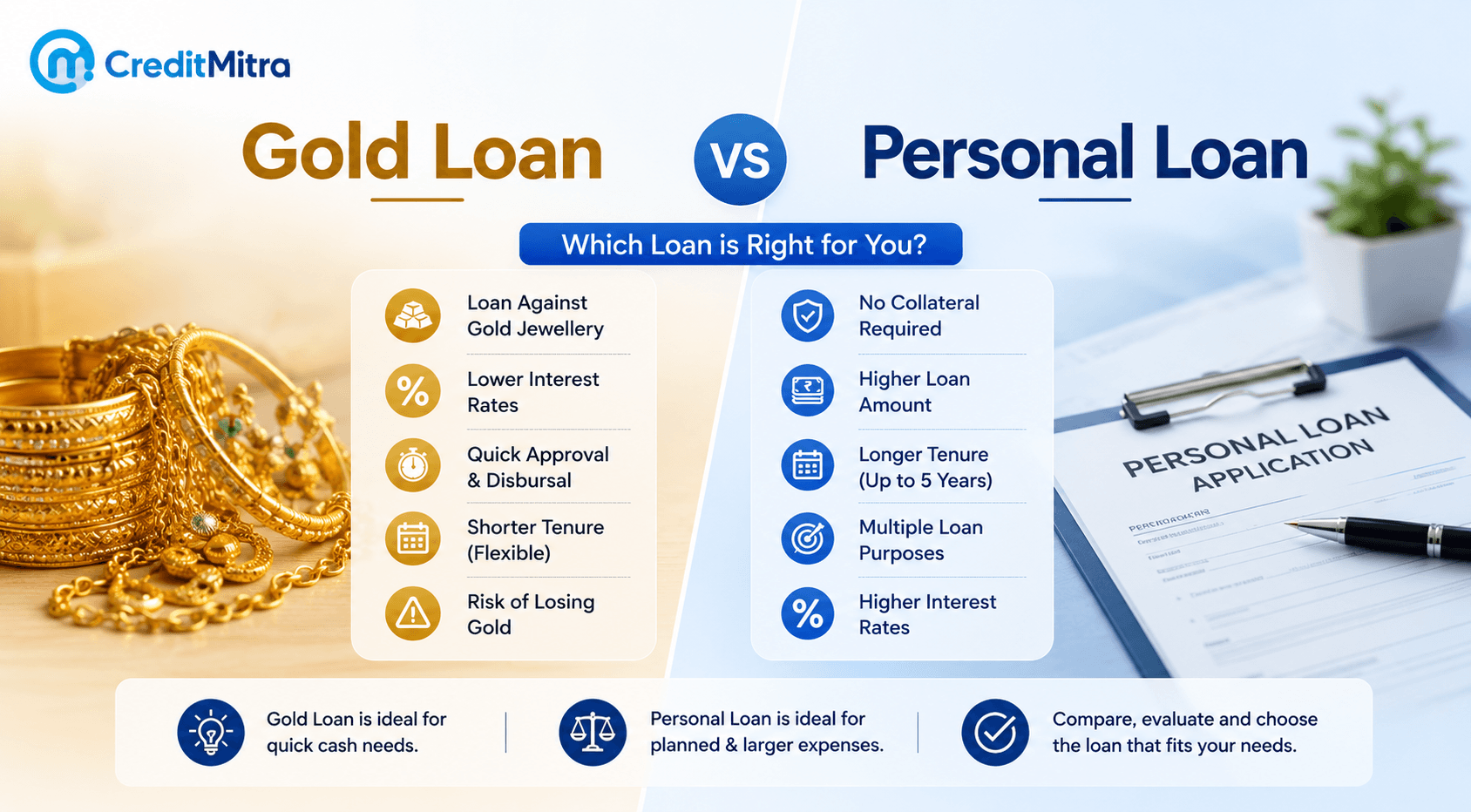

If Below 650:

- Gold loans better option than personal loan

- Wait 3 months, improve score, reapply

- Fintech might still approve (at high rates)

Final Takeaway

Checking your CIBIL score by PAN card in 2026 is:

- ✅ Free (once per year officially)

- ✅ Fast (5 minutes)

- ✅ Secure (OTP protects you)

- ✅ No score damage (soft inquiry)

- ✅ Essential before loan applications

Your action plan:

- Visit www.cibil.com

- Enter PAN details

- Verify with OTP

- Review your full credit report (not just score)

- Look for errors, dispute if found

- Use score to decide loan strategy

- Before applying, use CreditMitra to compare options without CIBIL damage

Your CIBIL score is your financial reputation. Check it regularly. Own it confidently.

Author

Best Travel Credit Cards No Fees in India 2026: Top 8 Lifetime-Free Cards Compared

Gold Loan vs Personal Loan in India 2026 – Which Is Better?