Gold Loan vs Personal Loan in India 2026 – Which Is Better?

Summarize with AI

You have ₹3 lakh emergency. Two options:

Option 1 (Gold Loan): Pledge 50 grams gold jewelry. Walk out with ₹3 lakh in 30 minutes. Cost: ₹22,500 interest (9% for 6 months). No CIBIL check.

Option 2 (Personal Loan): Apply with documents. Wait 2-5 days. Cost: ₹36,000 interest (13% for 6 months). CIBIL check required.

Gold loan saves ₹13,500 and 4 days. But there is one risk: lose gold if you don’t repay.

Here’s the complete breakdown to choose between them.

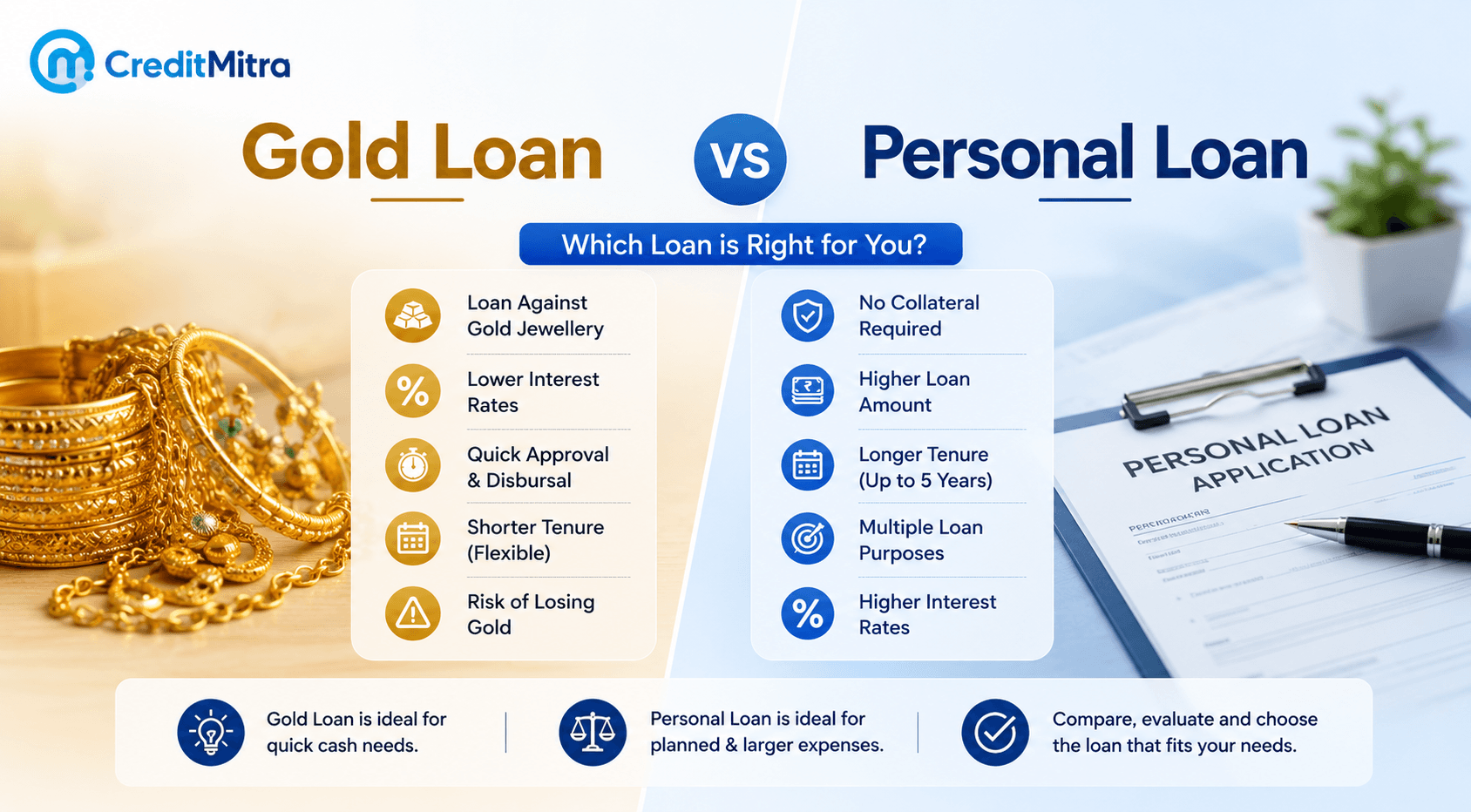

What’s the Difference?

Gold Loan:

- You pledge gold as collateral

- Lender evaluates purity/weight

- Instant money (30-60 minutes)

- Lower interest (7-14% p.a.)

- No CIBIL check

- No income proof required

- Loan amount: ₹20,000 to ₹50 lakh (based on gold)

- Tenure: 3-36 months

- Risk: Lose gold if you default

Personal Loan:

- Unsecured (no collateral)

- Based on income + CIBIL score

- Takes 2-5 days

- Higher interest (11-24% p.a.)

- CIBIL 700+ preferred

- Income proof required

- Loan amount: ₹50,000 to ₹40 lakh

- Tenure: 3-5 years

- No asset risk

Interest Rate Comparison (Real Cost Example)

Scenario: ₹5 lakh loan, 2 years

Gold Loan (Kotak 8%):

- Monthly EMI: ₹22,167

- Total interest: ₹32,000

- Total cost: ₹5,32,000

Personal Loan (HDFC 13%):

- Monthly EMI: ₹23,320

- Total interest: ₹59,680

- Total cost: ₹5,59,680

Savings with gold loan: ₹27,680 (5% cheaper)

For ₹1 lakh same terms:

- Gold loan (9%): Interest ₹9,750

- Personal loan (15%): Interest ₹16,300

- Savings: ₹6,550

The interest advantage is REAL and SUBSTANTIAL.

Speed Comparison

Gold Loan Timeline:

- Day 1: Visit branch, submit gold + KYC

- Day 1: Gold appraisal (15 minutes)

- Day 1: Money transferred (30-60 minutes TOTAL)

Personal Loan Timeline:

- Day 1-2: Online application

- Day 2-3: Income/employment verification

- Day 3-4: Credit check

- Day 4-5: Money transferred (3-5 days TOTAL)

Gold loans are 100-200x faster for emergency funds.

CIBIL & Eligibility Comparison

Gold Loan:

- No CIBIL score required

- No income proof needed

- No employment verification

- Age: 18-60 years

- Gold: 18-24 karat (min)

- Processing fee: ₹250-1,000

- Eligibility: Just bring gold + KYC

Personal Loan:

- CIBIL 700+ for best rates

- Income proof required (salary slips, ITR)

- Employment verification needed

- Age: 21-65 years typically

- Credit score: 650+ minimum

- Processing fee: ₹500-5,000

- Eligibility: Income + CIBIL + documents

For low CIBIL (500-650) borrowers: Gold loan is only option.

Maximum Loan Amount

Gold Loan:

- Based on gold pledged

- LTV: 75-85% of gold value

- Example: 100g gold at ₹7,200/gram = ₹7,20,000 × 75% = ₹5,40,000 max loan

- Formula: (Weight × Purity × Rate × LTV%)

Personal Loan:

- Based on income

- Formula: Income × 24 months ÷ Total existing EMI ratio

- Example: ₹35,000 income, no existing EMI = ₹3-5 lakh loan possible

- Max: Can be ₹40-50 lakh for high earners

For large amounts (>₹10 lakh): Personal loan better (gold-based limited).

Tenure (Repayment Period)

Gold Loan:

- 3 months to 36 months maximum

- Most common: 6-12 months

- Short-term borrowing only

- Flexible repayment (interest-only, bullet, EMI)

Personal Loan:

- 12 months to 60+ months

- Most common: 3-5 years

- Long-term borrowing

- Fixed monthly EMI only

For long-term needs (3+ years): Personal loan better (lower monthly burden).

Real Scenario: When Gold Loan Wins

Example Profile:

- Age: 35

- Monthly income: ₹20,000 (self-employed)

- CIBIL: 580 (poor credit history)

- Emergency: ₹2 lakh needed immediately

- Gold available: 100 grams 22-karat

Gold Loan Option:

- Loan amount: ₹1.5-2 lakh

- Rate: 10% (NBFCs accept low credit)

- Processing: 30 minutes

- Approval: 100% certain

- Monthly EMI (12 months): ₹17,500

Personal Loan Option:

- Application: REJECTED (CIBIL 580 too low)

- No option available

- Result: Gold loan ONLY viable choice

Real Scenario: When Personal Loan Wins

Example Profile:

- Age: 28

- Monthly income: ₹75,000

- CIBIL: 750 (excellent)

- Need: ₹8 lakh for home renovation

- Gold available: 50 grams only

Gold Loan Option:

- Maximum loan: ₹3-4 lakh (50g gold insufficient)

- Cannot meet ₹8 lakh need

- Option not viable

Personal Loan Option:

- Loan amount: ₹8 lakh approved

- Rate: 10.5% (excellent CIBIL)

- Processing: 3 days

- Monthly EMI (5 years): ₹17,000

- Result: Personal loan ONLY viable choice

Decision Framework

Choose Gold Loan If:

- Need money urgently (<1 hour)

- Have gold jewelry available

- CIBIL score <650

- Loan amount <₹5 lakh

- Can repay within 12-24 months

- Want lowest interest cost

- Don’t mind pledging gold

Choose Personal Loan If:

- CIBIL score >700

- Need >₹5 lakh

- Don’t want to pledge assets

- Need 3-5 year repayment

- Want consistent monthly EMI

- Salaried with income proof

- Risk-averse on gold loss

FAQ

Q: Can I take both a gold loan and a personal loan simultaneously?

A: Yes. But lenders check total debt. Both must fit within your FOIR (debt/income <50%).

Q: If I default on a gold loan, what happens?

A: Lender sends notice, gives grace period. If you still don’t pay, gold is auctioned. Surplus returned to you. Default reported to CIBIL.

Q: Does gold loan affect my personal loan eligibility?

A: No, not directly. But lenders check all outstanding loans when evaluating debt capacity.

Q: Which is safer—pledging gold or pledging creditworthiness?

A: Gold is tangible (safer for lenders). A personal loan relies on your repayment discipline (you control risk). Both are safe if you repay on time.

Q: Can I take a gold loan for any purpose?

A: Yes. No restriction. Medical, education, emergency, home renovation—any purpose allowed.

Q: How is gold valued for loan?

A: Lender uses certified assayer, RBI reference rate, and applies purity factor. 18K worth <22K worth <24K. Hallmarked gold gets full weight; non-hallmarked gold gets 5-15% discount.

Conclusion: Gold Loan for Emergencies, Personal Loan for Planning

Gold Loan Wins For:

- Emergency funds needed NOW

- Low/poor CIBIL score

- Minimal documentation desire

- Short-term (6-12 months)

- Interest cost priority

- Self-employed professionals

Personal Loan Wins For:

- Planned large purchases

- Excellent CIBIL (750+)

- Long-term needs (3-5 years)

- Large amounts (>₹5 lakh)

- Salaried employees

- No asset risk preference

For Most Indians: If emergency and have gold → Gold loan. If planned expense and good CIBIL → Personal loan.

Use CreditMitra to compare personal loan options (soft inquiry protects CIBIL). Compare gold loan rates at 2-3 banks simultaneously. Choose based on YOUR specific situation, not generic “best.”

The right choice isn’t about one being universally better—it’s about which fits your situation perfectly.

Author

Personal Loan for Contract Employees: Complete Guide to Getting Approved (2026)

ICICI Bank Balance Check Number: All Methods to Check Balance Instantly